"In investing what is comfortable is rarely profitable."

USD

EUR/USD

The Shared currency rallied to a high $1.1120 yesterday after the ECB surprisingly stated it would end the Asset Purchase Program (APP) in the third quarter but the pair quickly pared all gains to $1.1000 in the absence of a positive outcome from the peace talks in Turkey and a weaker economic growth.

GBP/USD

The Cable dropped to a fresh 52-week low at $ 1.3085 as a fresh wave in risk aversion forced investors to sell the pound. Market eyes for GBP and Manufacturing data.

USD/JPY

The Japanese yen nosedived to 116.60 undermined by higher US yields and better than expected data from the US.

AUD/USD

The Aussie dollar headed higher to $0.7351 as Russian-Ukraine conflict kept commodity prices elevated, and on comments from Reserve Bank of Australia Philip Low that domestic growth would be quite strong this year.

USD/CAD

The Loonie oscillated between 1.2750- 12780 against the greenback ahead of Canada's Unemployment rate later today.

USD/ZAR

South African rand stayed put around 15.04 despite USD strength amid hope of domestic economic recovery.

USD/MUR

The dollar-rupee remained unchanged at 43.70 (Selling).

11:00 - GBP - Gross Domestic Product

13:30 - GBP - Consumer inflation expectations

17:30 - CAD - Unemployment rate

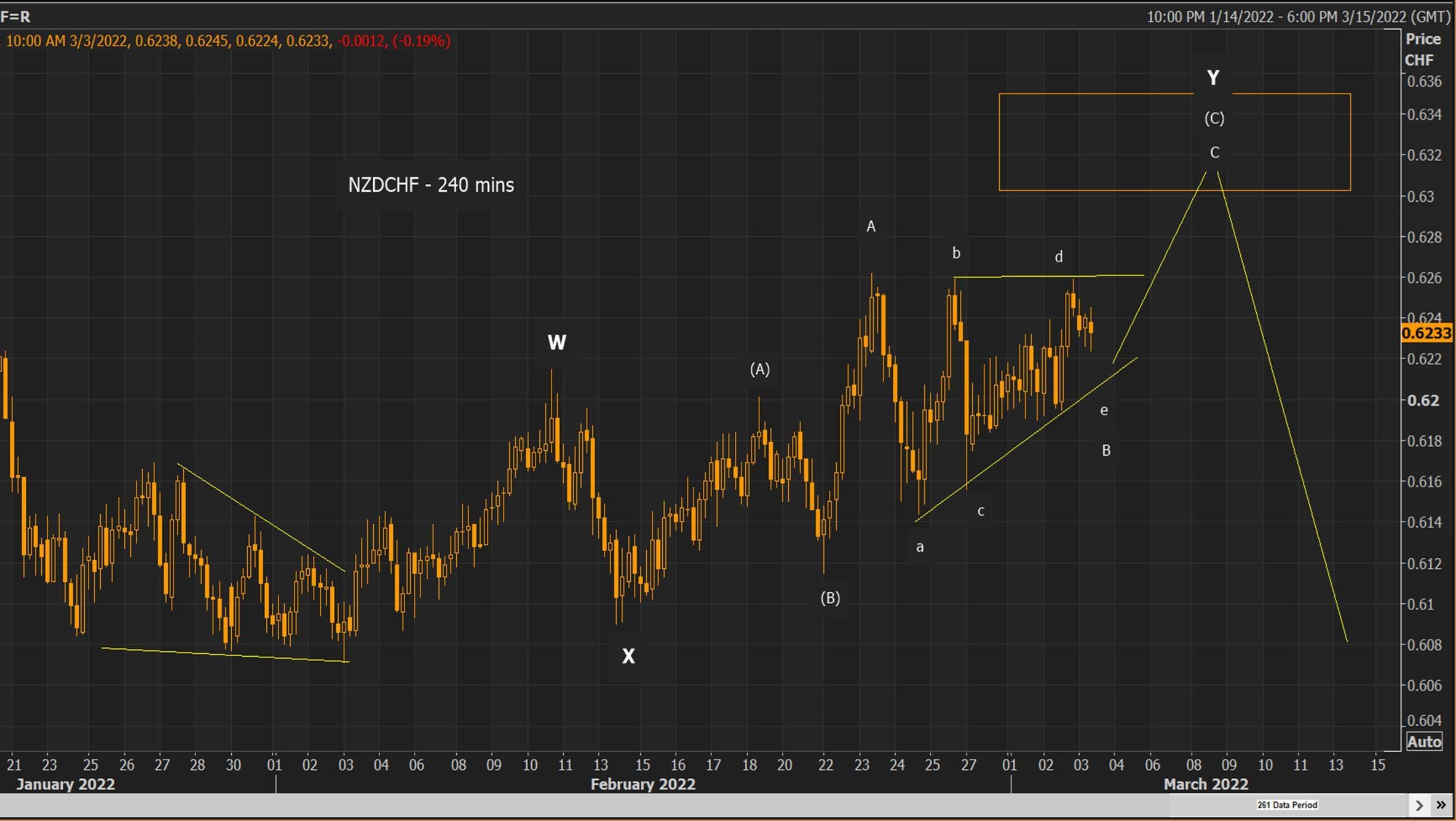

After bouncing back from key resistance level 0.6262 from the upside as per our last forecast (see below) , NZDCHF sworn down to 0.6144 but lacked sufficient selling pressure to continue its downtrend.

It appears that final wave Y of W-X-Y correction is quite complex and there might be 2 scenarios popping up in the near term.

Scenario 1 : we could have reached final wave ‘e’ before downtrend resumes. (As per Elliott wave principle a triangle can be formed as final wave C of wave Y of W-X-Y correction)

Key resistance level is wave ‘e’ of barrier triangle of wave C – 0.6259.