“Internal audit teams should be in a position to express their views at any stage”

Published on

May 03, 2019

Published in Category

Expert views

Successful internal auditors preserve and create value amidst a changing banking landscape. However, says Kristy Ballah, Head of Audit at AfrAsia Bank, value creation is achievable when the internal audit team can develop additional synergy with other controls functions of the organization, communication and sharing. Over the years, they had a general tendency to refrain from giving insights and challenge management on projects or major decisions.

What are the regulator’s expectations of the internal audit function?

They are high expectations which include providing independent assurance to the board and senior management on whether (i) the internal control system in place is performing effectively and is adequate to mitigate risks consistent with the risk appetite of the financial institution, (ii) the organizational goals are met and corporate governance processes are effective and efficient.To achieve this, competent people have to be recruited and given the cost involved, internal auditors should play a vital role in the process of value preservation and creation.

What are the main elements that are changing the banking landscape?

Some emerging factors are heavily impacting the banking landscape posing considerable challenges to banks. For instance, the needs of customers have evolved and are becoming more complex and sophisticated which require banks to leverage to a much bigger extent on Fintech. Open banking which is making way for more competition and cloud computing are other essential elements that considerably impact international banking on the technology front.Cost of compliance has risen significantly across the globe. The attempt to improve AML-CFT programs after several reputable banks have been heavily fined by regulators in recent years for non-conformity with AML-CFT requirements and higher regulations coming into play since the financial crisis are the main reasons. Cybercrime and societal pressure for more responsible banking that align the bank’s strategy to society goals are also among the most topical items.As a result, banks are having to frequently revise their strategic orientations which impacts the internal auditor’s agenda. The traditional control focused approach has to change to meet the broader expectations of key stakeholders.

How can the internal auditor preserve value in this context?

First of all, he shall be more than ever strategy-oriented and have a sound knowledge of the organization’s and departmental objectives. This enables a more holistic view which is helpful in formulating recommendations on the alignment of people, systems, structure and processes with the business strategy and values of the organization. A more stringent methodology and structured approach shall be adopted to produce the risk-based internal audit plan so that areas necessitating most audit efforts are identified upfront and prioritized. The financial implication of the process to be audited, the corresponding volume of transactions, whether regulatory requirements are applicable and whether changes have occurred in management, structure and systems are among the factors that should compulsorily be taken into account and critically rated. The plan shall also take into account elements from the bank’s risk register and remain dynamic so that changes in the year can be adequately reflected. Moreover, the internal auditor shall not only satisfy himself that a control is being performed or process is followed as was done traditionally. He has room and also a duty to propose ways to reduce the cost of control performance highlighting duplications and complexity that could be eliminated or recommending automation after undertaking relevant cost benefit analysis having regard to the portfolio of controls. To a greater extent, internal audit teams should recommend investments in digital assets so that the lion share of core assurance becomes automated, hence the monitoring of controls and flagging of non-conformance will be done real time. Value preservation is therefore achievable but the internal auditor must go the extra mile and explore the possibility of value creation.

Is there any room for value creation?

Value creation is achievable provided the internal audit team can develop additional synergy with other controls functions of the bank such as Risk and Compliance, through enhanced communication, sharing of work plans and joint assignments where relevant. Without this initiative, there will be no consolidated bank-wide view of governance issues and risk and mitigation will not be effective since risk identification, measurement and monitoring will be influenced by departmental objectives without paying attention to the bigger picture. Having a better synergy among the control functions will also encourage more risk anticipation whereby the key players will use their professional judgment and analytics to identify emerging risks in a timelier manner.Internal auditors can dare which will create opportunities to add value. Over the years, they had a general tendency to refrain from giving insights and challenge management on projects or major decisions fearing this may conflict and cause independence issues when they will audit same at a later stage. Internal audit teams should be in a position to express their views at any stage provided same can be supported by facts and spot on examples from past experience. The internal audit team can be involved earlier on projects as this results in numerous benefits to the organization considering that better project governance will be encouraged from the outset and corrective actions can be taken before resources are consumed. The merits will be bigger when the organization is not very mature in the delivery of major projects and is about to embark on an internal transformation exercise such as digitalization. There are other tasks that can contribute to adding value. For instance, internal auditors can assign an even bigger priority to high fraud risk areas in audit planning and also ensure the designated audit process comprise more forensic techniques though fraud management is not the internal auditor’s primary duty. The internal audit team can also, amongst others, assist management in undertaking follow ups on the implementation of the external auditor’s management letter or regulators’ inspection report and provide independent periodic updates to management.

Which attributes shall the internal auditor display in this disruptive banking environment?

The internal auditor shall be highly agile. He needs to display open mindedness and skepticism, be courageous to speak the truth to power and be future oriented in the attempt to anticipate risks and take mitigating action. The internal auditor must also constantly upskill/reskill in this technology era to supplement available business skills and acumen. The internal audit team must be visible and find means to communicate and market any value add they are bringing, using quantification wherever possible. This will boost relationships with key stakeholders and act as justification that the internal auditor is a Trusted Advisor who deserves a seat at the table. To conclude, the extent to which the internal auditor can readapt his agenda in the light of the disruptive banking environment and implement it will determine how successful he is.

Expert views

January 20, 2026

What is the right investment strategy for you?

Expert views

January 20, 2026

What is the right investment strategy for you?

Expert views

October 22, 2025

Mauritius–UAE: A Strategic Bridge to Africa

Expert views

October 22, 2025

Mauritius–UAE: A Strategic Bridge to Africa

Expert views

August 14, 2024

Mauritius as a gateway for investment and transfer of capacity to Africa.

Expert views

August 14, 2024

Mauritius as a gateway for investment and transfer of capacity to Africa.

Expert views

July 26, 2024

We have seen a marked increase in initiatives aimed at supporting women’s entry and advancement in the finance industry.

Expert views

July 26, 2024

We have seen a marked increase in initiatives aimed at supporting women’s entry and advancement in the finance industry.

Expert views

June 11, 2024

With Africa’s projected continued growth, a robust banking network is crucial.

Expert views

June 11, 2024

With Africa’s projected continued growth, a robust banking network is crucial.

Expert views

March 15, 2024

Tailored Financial Excellence: Mauritius’ Unique Investor Advantages

Expert views

March 15, 2024

Tailored Financial Excellence: Mauritius’ Unique Investor Advantages

Expert views

May 11, 2023

Banking on sustainable finance to scale up the Mauritius IFC

Expert views

May 11, 2023

Banking on sustainable finance to scale up the Mauritius IFC

Expert views

May 10, 2023

Mauritius & South Africa: A mutually beneficial trade relationship

Expert views

May 10, 2023

Mauritius & South Africa: A mutually beneficial trade relationship

Expert views

April 17, 2023

Mauritius IFC: From a conventional jurisdiction to a forward-looking hub

Expert views

April 17, 2023

Mauritius IFC: From a conventional jurisdiction to a forward-looking hub

Golf

December 18, 2022

Record win for Rozner in AfrAsia Bank Mauritius Open

Golf

December 18, 2022

Record win for Rozner in AfrAsia Bank Mauritius Open

Golf

December 17, 2022

Rozner chasing AfrAsia Bank Mauritius Open glory

Golf

December 17, 2022

Rozner chasing AfrAsia Bank Mauritius Open glory

Golf

December 16, 2022

Rozner in the hunt again at AfrAsia Bank Mauritius Open

Golf

December 16, 2022

Rozner in the hunt again at AfrAsia Bank Mauritius Open

Golf

December 15, 2022

Course record for Välimäki to lead AfrAsia Bank Mauritius Open

Golf

December 15, 2022

Course record for Välimäki to lead AfrAsia Bank Mauritius Open

Expert views

December 01, 2022

Africa’s Drive Towards Sustainability: Launch of ESG GPS in Mauritius

Expert views

December 01, 2022

Africa’s Drive Towards Sustainability: Launch of ESG GPS in Mauritius

Expert views

October 20, 2022

Quelle est l'influence des taux d'intérêt sur le prix de l'or?

Expert views

October 20, 2022

Quelle est l'influence des taux d'intérêt sur le prix de l'or?

Golf

October 18, 2022

Mont Choisy Le Golf set to impress as host of 2022 AfrAsia Bank Mauritius Open

Golf

October 18, 2022

Mont Choisy Le Golf set to impress as host of 2022 AfrAsia Bank Mauritius Open

Golf

September 16, 2022

Burmester confirmed for 2022 AfrAsia Bank Mauritius Open

Golf

September 16, 2022

Burmester confirmed for 2022 AfrAsia Bank Mauritius Open

Expert views

July 28, 2022

EUR/USD – la roupie prise en étau

Expert views

July 28, 2022

EUR/USD – la roupie prise en étau

Expert views

June 01, 2022

Africa CEO Forum 2022 - Malachy McAllister on CNBC Africa

Expert views

June 01, 2022

Africa CEO Forum 2022 - Malachy McAllister on CNBC Africa

Differentiate. Inspire. Celebrate

April 29, 2022

AfrAsia Bank further sharpens its expertise with Elliott Wave Certification

Differentiate. Inspire. Celebrate

April 29, 2022

AfrAsia Bank further sharpens its expertise with Elliott Wave Certification

Expert views

March 04, 2022

Journée des droits des femmes: STOP aux freins invisibles

Expert views

March 04, 2022

Journée des droits des femmes: STOP aux freins invisibles

Expert views

March 04, 2022

The real opportunity and uniqueness of Mauritius lies in its diversified economic landscape with opportunities in various sectors.

Expert views

March 04, 2022

The real opportunity and uniqueness of Mauritius lies in its diversified economic landscape with opportunities in various sectors.

Expert views

March 02, 2022

La crise Russie-Ukraine : Quels sont les enjeux financiers à prévoir ?

Expert views

March 02, 2022

La crise Russie-Ukraine : Quels sont les enjeux financiers à prévoir ?

Testimonials

February 08, 2022

'AfrAsia Bank has always been a trusted financial partner for us.'

Testimonials

February 08, 2022

'AfrAsia Bank has always been a trusted financial partner for us.'

Testimonials

February 08, 2022

“ Their legacy-building ethos and customer service structure resonates with us.”

Testimonials

February 08, 2022

“ Their legacy-building ethos and customer service structure resonates with us.”

Expert views

January 19, 2022

Preserving the human touch in banking in the digital age

Expert views

January 19, 2022

Preserving the human touch in banking in the digital age

Expert views

November 22, 2021

Mauritius is back in business – What to expect for the Tourism/Hospitality and Real Estate sectors?

Expert views

November 22, 2021

Mauritius is back in business – What to expect for the Tourism/Hospitality and Real Estate sectors?

Expert views

November 22, 2021

A new era for the Mauritius IFC

Expert views

November 22, 2021

A new era for the Mauritius IFC

Expert views

November 22, 2021

A Purposeful Brand - It's not about 'I', it's about 'We'

Expert views

November 22, 2021

A Purposeful Brand - It's not about 'I', it's about 'We'

Expert views

November 03, 2021

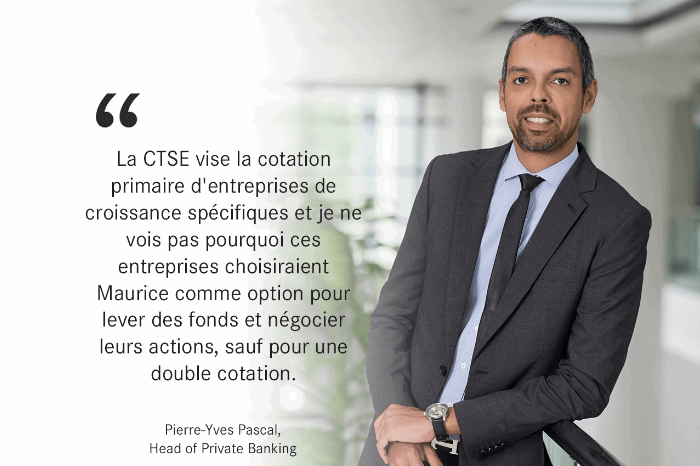

Quels sont les enjeux pour la Bourse de Maurice avec l’arrivée du Cape Town Stock Exchange ?

Expert views

November 03, 2021

Quels sont les enjeux pour la Bourse de Maurice avec l’arrivée du Cape Town Stock Exchange ?

Expert views

October 20, 2021

#Stagflation : Comment s’adapter à cet nouvel ordre économique ?

Expert views

October 20, 2021

#Stagflation : Comment s’adapter à cet nouvel ordre économique ?

Expert views

October 20, 2021

Fonds d’investissements : Est-ce le moment d’investir ?

Expert views

October 20, 2021

Fonds d’investissements : Est-ce le moment d’investir ?

Expert views

October 18, 2021

Marché des changes: Quel est l’impact sur nos réserves en devises étrangères ?

Expert views

October 18, 2021

Marché des changes: Quel est l’impact sur nos réserves en devises étrangères ?

Expert views

September 15, 2021

« Le marché de la banque privée est amené a plus que doubler au cours des cinq prochaines années »

Expert views

September 15, 2021

« Le marché de la banque privée est amené a plus que doubler au cours des cinq prochaines années »

Expert views

September 01, 2021

Rather than a purely government or business matter, country branding is more of a concerted and integrated effort made by all stakeholders, including the population.

Expert views

September 01, 2021

Rather than a purely government or business matter, country branding is more of a concerted and integrated effort made by all stakeholders, including the population.

Expert views

August 11, 2021

More activities expected between India and Africa via Mauritius

Expert views

August 11, 2021

More activities expected between India and Africa via Mauritius

Expert views

August 04, 2021

Repo Rate à 1.85% - Maintenir la tendance baissière des 5 dernières années ou pas ?

Expert views

August 04, 2021

Repo Rate à 1.85% - Maintenir la tendance baissière des 5 dernières années ou pas ?

Expert views

August 01, 2021

What is a Structured Product?

Expert views

August 01, 2021

What is a Structured Product?

Expert views

July 14, 2021

Global Battery Market powered by Automotive Electrification - Structured Product

Expert views

July 14, 2021

Global Battery Market powered by Automotive Electrification - Structured Product

Expert views

July 13, 2021

Deepening our Expertise to serve you better

Expert views

July 13, 2021

Deepening our Expertise to serve you better

Expert views

July 12, 2021

Meet our new Head of Sustainability and CSR, Alvin Peerthy

Expert views

July 12, 2021

Meet our new Head of Sustainability and CSR, Alvin Peerthy

Expert views

July 05, 2021

The Mauritian Rupee faces the COVID-19 brunt

Expert views

July 05, 2021

The Mauritian Rupee faces the COVID-19 brunt

Events & Webinar

June 30, 2021

#Webinar Replay: Cross-border opportunities and challenges in Africa

Events & Webinar

June 30, 2021

#Webinar Replay: Cross-border opportunities and challenges in Africa

Events & Webinar

June 14, 2021

20 Min with AfrAsia Webinar - Digital Transformation to build a Sustainable Business

Events & Webinar

June 14, 2021

20 Min with AfrAsia Webinar - Digital Transformation to build a Sustainable Business

Expert views

June 09, 2021

Millionaires in Africa: an attractive market for Mauritius

Expert views

June 09, 2021

Millionaires in Africa: an attractive market for Mauritius

Expert views

June 07, 2021

La charge est-elle équitablement partagée entre l’Étate et le privé?

Expert views

June 07, 2021

La charge est-elle équitablement partagée entre l’Étate et le privé?

Expert views

May 26, 2021

The revival of the UK-Mauritius trade together with the tourism sector could generate more revenue and appreciate the Mauritian rupee

Expert views

May 26, 2021

The revival of the UK-Mauritius trade together with the tourism sector could generate more revenue and appreciate the Mauritian rupee

Expert views

May 21, 2021

Tant que nos frontières restent fermées, cette pénurie devrait se poursuivre dans le proche avenir.

Expert views

May 21, 2021

Tant que nos frontières restent fermées, cette pénurie devrait se poursuivre dans le proche avenir.

Events & Webinar

May 21, 2021

Retour sur notre #webinaire : Gestion de patrimoine - Post COVID

Events & Webinar

May 21, 2021

Retour sur notre #webinaire : Gestion de patrimoine - Post COVID

Expert views

May 19, 2021

Local customers represent 70% of these assets.

Expert views

May 19, 2021

Local customers represent 70% of these assets.

Expert views

May 13, 2021

Global vaccination campaign, Inflation and Financial Assets – let’s talk!

Expert views

May 13, 2021

Global vaccination campaign, Inflation and Financial Assets – let’s talk!

Expert views

May 12, 2021

Automotive Electrification and the Global Battery Market – are Nickel, Copper and Aluminium your next investment opportunity?

Expert views

May 12, 2021

Automotive Electrification and the Global Battery Market – are Nickel, Copper and Aluminium your next investment opportunity?

Expert views

May 11, 2021

Cybersecurity Awakening

Expert views

May 11, 2021

Cybersecurity Awakening

Events & Webinar

April 07, 2021

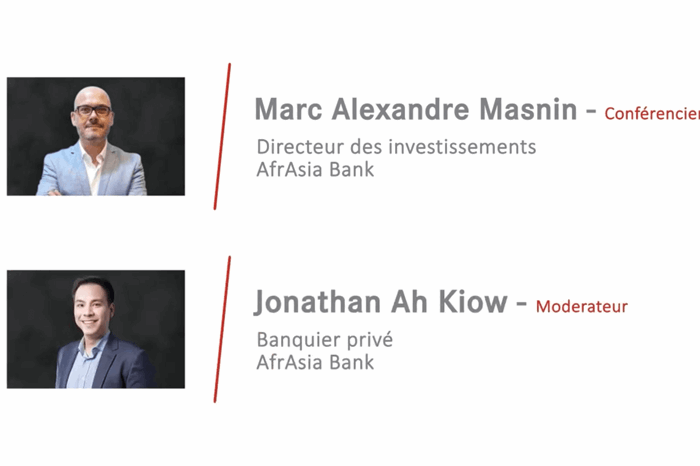

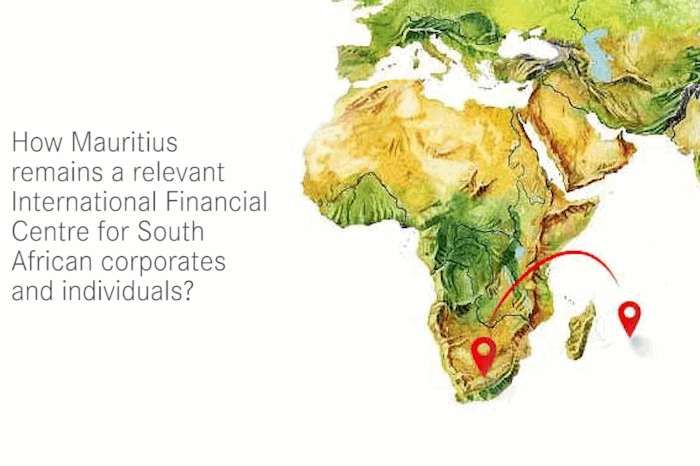

How Mauritius remains a relevant IFC for South African Corporates & Individuals?

Events & Webinar

April 07, 2021

How Mauritius remains a relevant IFC for South African Corporates & Individuals?

Expert views

March 24, 2021

Marc-Alexandre Masnin, Directeur des investissements - Business Magazine

Expert views

March 24, 2021

Marc-Alexandre Masnin, Directeur des investissements - Business Magazine

Expert views

March 24, 2021

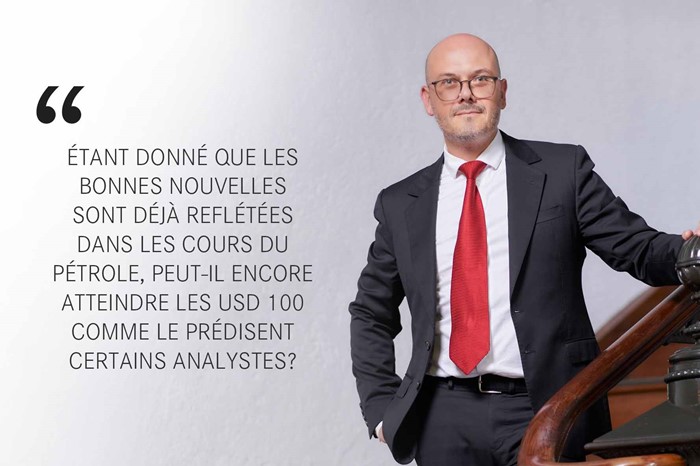

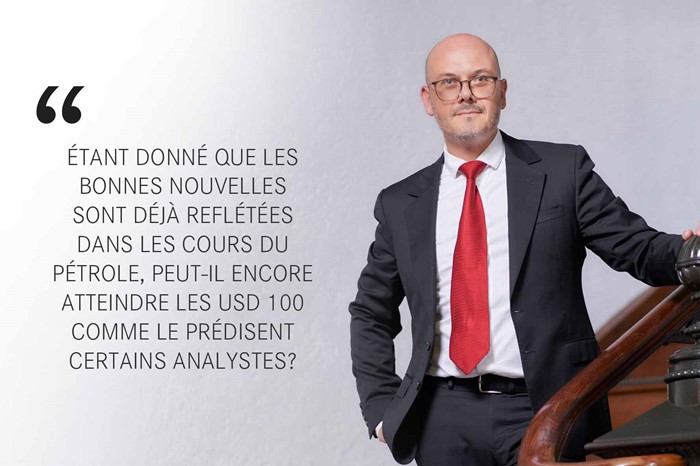

At the height of the crisis last year, the price of the oil barrel turned negative. However, it hovers today above 60 dollars. Is this a show of confidence in a faster economic recovery?

Expert views

March 24, 2021

At the height of the crisis last year, the price of the oil barrel turned negative. However, it hovers today above 60 dollars. Is this a show of confidence in a faster economic recovery?

Community

March 18, 2021

#InternationalWomensDay: Do you Choose to Challenge?

Community

March 18, 2021

#InternationalWomensDay: Do you Choose to Challenge?

Expert views

March 17, 2021

L’économie mauricienne peut-elle survivre à un deuxième confinement ?

Expert views

March 17, 2021

L’économie mauricienne peut-elle survivre à un deuxième confinement ?

Community

March 08, 2021

#InternationalWomensDay: Do you Choose to Challenge?

Community

March 08, 2021

#InternationalWomensDay: Do you Choose to Challenge?

The Believers in Local

February 16, 2021

#AfrAsiaBankLocalMarket – Chinese New Year & Valentine’s Day

The Believers in Local

February 16, 2021

#AfrAsiaBankLocalMarket – Chinese New Year & Valentine’s Day

Expert views

February 11, 2021

Interview with Robin Smither, Senior Executive, Head of Corporate Banking, AfrAsia Bank

Expert views

February 11, 2021

Interview with Robin Smither, Senior Executive, Head of Corporate Banking, AfrAsia Bank

Expert views

February 03, 2021

Jolene Li Sing How, one of the very first Certified Elliott Wave Analysts

Expert views

February 03, 2021

Jolene Li Sing How, one of the very first Certified Elliott Wave Analysts

Expert views

January 20, 2021

AfrAsia was awarded two distinctions by Elliott Wave International.

Expert views

January 20, 2021

AfrAsia was awarded two distinctions by Elliott Wave International.

The Believers in Local

December 23, 2020

The believers in local - Christmas Market

The Believers in Local

December 23, 2020

The believers in local - Christmas Market

Expert views

December 16, 2020

Mauritius on the EU Black List, what impact since October 1st, 2020?

Expert views

December 16, 2020

Mauritius on the EU Black List, what impact since October 1st, 2020?

Expert views

December 14, 2020

Marché des cartes – la dématérialisation enclenchée

Expert views

December 14, 2020

Marché des cartes – la dématérialisation enclenchée

Events & Webinar

December 09, 2020

How does Mauritius remain a relevant International Financial Centre for South African corporates and individuals?

Events & Webinar

December 09, 2020

How does Mauritius remain a relevant International Financial Centre for South African corporates and individuals?

Expert views

November 18, 2020

«Face aux incertitudes actuelles, privilégier une approche core-satellite»

Expert views

November 18, 2020

«Face aux incertitudes actuelles, privilégier une approche core-satellite»

Expert views

November 18, 2020

Nantes Lavin interview on Business Mag

Expert views

November 18, 2020

Nantes Lavin interview on Business Mag

Expert views

October 29, 2020

ESG and Responsible Investments – Breaking through to shape a Sustainable World

Expert views

October 29, 2020

ESG and Responsible Investments – Breaking through to shape a Sustainable World

Expert views

October 28, 2020

Is Biden winning the forthcoming US Presidential Elections?

Expert views

October 28, 2020

Is Biden winning the forthcoming US Presidential Elections?

Expert views

October 27, 2020

Global Wealth Migration Review 2020

Expert views

October 27, 2020

Global Wealth Migration Review 2020

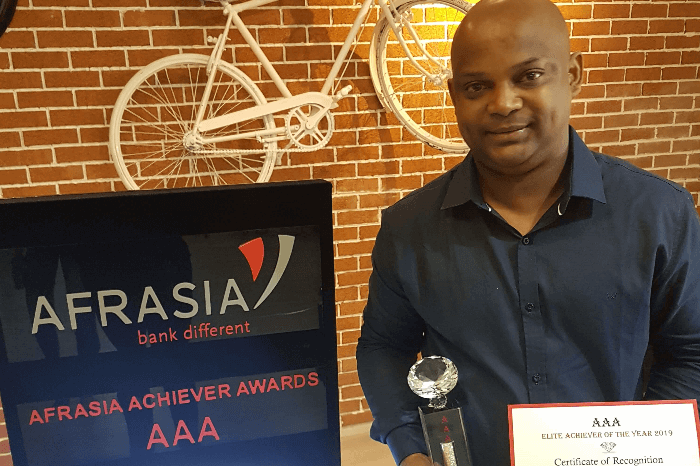

Differentiate. Inspire. Celebrate

October 26, 2020

Meet David Chamtyoo, our Elite Achiever of the Year 2019

Differentiate. Inspire. Celebrate

October 26, 2020

Meet David Chamtyoo, our Elite Achiever of the Year 2019

The Believers in Local

October 26, 2020

Our very first Local Market

The Believers in Local

October 26, 2020

Our very first Local Market

Expert views

October 21, 2020

The best international managers have lost money"

Expert views

October 21, 2020

The best international managers have lost money"

Expert views

October 14, 2020

Étant à ce jour «Covid-free», l’île Maurice jouit-elle d’un écosystème robuste pour assurer la protection de vos actifs?

Expert views

October 14, 2020

Étant à ce jour «Covid-free», l’île Maurice jouit-elle d’un écosystème robuste pour assurer la protection de vos actifs?

Events & Webinar

October 07, 2020

20 min with AfrAsia - Environment, Social & Governance (ESG) and Responsible Investments

Events & Webinar

October 07, 2020

20 min with AfrAsia - Environment, Social & Governance (ESG) and Responsible Investments

Expert views

September 30, 2020

The inclusion of Mauritius on the European Union's blacklist is a considerable hindrance to the image of our international financial center.

Expert views

September 30, 2020

The inclusion of Mauritius on the European Union's blacklist is a considerable hindrance to the image of our international financial center.

Events & Webinar

September 24, 2020

Webinar : Foreigners taking up Mauritian Tax Residency – Should they be worried about their Mauritian Trust?

Events & Webinar

September 24, 2020

Webinar : Foreigners taking up Mauritian Tax Residency – Should they be worried about their Mauritian Trust?

Expert views

September 21, 2020

Luvna Arnassalon-Seerungen: “Covid-19 has further put sustainability under the corporate spotlight”

Expert views

September 21, 2020

Luvna Arnassalon-Seerungen: “Covid-19 has further put sustainability under the corporate spotlight”

Expert views

September 17, 2020

Boosting Mauritius’ reputation as a key enabler of trade

Expert views

September 17, 2020

Boosting Mauritius’ reputation as a key enabler of trade

Business & Innovation

September 10, 2020

AfrAsia Customer Survey 2020

Business & Innovation

September 10, 2020

AfrAsia Customer Survey 2020

Expert views

September 08, 2020

Le Défi Quotidien : Marc-Alexandre Masnin, Head of Wealth Management- International / Investment Sales, AfrAsia Bank

Expert views

September 08, 2020

Le Défi Quotidien : Marc-Alexandre Masnin, Head of Wealth Management- International / Investment Sales, AfrAsia Bank

The Believers in Local

August 21, 2020

Believers in the passion of our entrepreneurs

The Believers in Local

August 21, 2020

Believers in the passion of our entrepreneurs

Expert views

August 19, 2020

Rakesh Seesurn, Head of Risk in Business Mag

Expert views

August 19, 2020

Rakesh Seesurn, Head of Risk in Business Mag

Expert views

August 18, 2020

Mauritius remains the best gateway for cross-border investments into Africa.

Expert views

August 18, 2020

Mauritius remains the best gateway for cross-border investments into Africa.

Events & Webinar

July 27, 2020

20 min with AfrAsia - Mauritius: More than just a property investment.

Events & Webinar

July 27, 2020

20 min with AfrAsia - Mauritius: More than just a property investment.

Expert views

July 01, 2020

Impacts of COVID-19 on South African Economy

Expert views

July 01, 2020

Impacts of COVID-19 on South African Economy

Expert views

July 01, 2020

Blue economy aims at generating multiple cash-flows from a portfolio of local opportunities

Expert views

July 01, 2020

Blue economy aims at generating multiple cash-flows from a portfolio of local opportunities

Community

July 01, 2020

Education remains key to success, even in a different normal

Community

July 01, 2020

Education remains key to success, even in a different normal

Expert views

June 29, 2020

EU blacklist: highly prejudicial to the economy

Expert views

June 29, 2020

EU blacklist: highly prejudicial to the economy

The Believers in Local

June 22, 2020

Believers in the authenticity of our talents

The Believers in Local

June 22, 2020

Believers in the authenticity of our talents

Expert views

June 08, 2020

As businesses undergo digital transformations in their front and back office operations, similarly cybercriminals are advancing the sophistication of their methods.

Expert views

June 08, 2020

As businesses undergo digital transformations in their front and back office operations, similarly cybercriminals are advancing the sophistication of their methods.

Expert views

June 06, 2020

The difference in taxation of foreign residents and Mauritian residents in the case of the Solidarity Levy is a first for the country

Expert views

June 06, 2020

The difference in taxation of foreign residents and Mauritian residents in the case of the Solidarity Levy is a first for the country

Community

June 01, 2020

Happy Mothers’ and Fathers’ Day!

Community

June 01, 2020

Happy Mothers’ and Fathers’ Day!

Expert views

May 21, 2020

Managing credit risks diligently

Expert views

May 21, 2020

Managing credit risks diligently

Expert views

May 21, 2020

In our opinion, the most impacted sector of the economy at this stage is the hospitality and tourism industry.

Expert views

May 21, 2020

In our opinion, the most impacted sector of the economy at this stage is the hospitality and tourism industry.

Expert views

May 20, 2020

A coordinated response to the impact of the crisis.

Expert views

May 20, 2020

A coordinated response to the impact of the crisis.

Expert views

May 08, 2020

COVID-19 - Operational Challenges v/s Technological Opportunities

Expert views

May 08, 2020

COVID-19 - Operational Challenges v/s Technological Opportunities

Expert views

May 07, 2020

“Converting the central bank into a magical money tree could lead to a significant currency devaluation”

Expert views

May 07, 2020

“Converting the central bank into a magical money tree could lead to a significant currency devaluation”

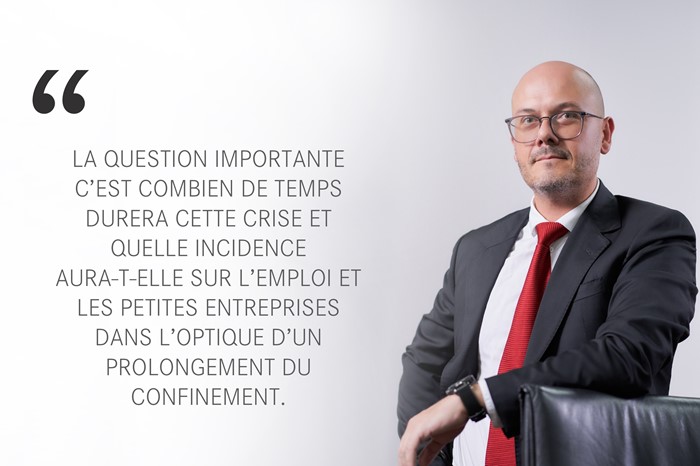

Expert views

May 06, 2020

“Banks will need to review their internal audit system”

Expert views

May 06, 2020

“Banks will need to review their internal audit system”

Expert views

April 27, 2020

Mastering market volatility is a key determinant for investors.

Expert views

April 27, 2020

Mastering market volatility is a key determinant for investors.

Expert views

April 22, 2020

Banks have a key role to play in economic recovery

Expert views

April 22, 2020

Banks have a key role to play in economic recovery

Expert views

April 20, 2020

Mauritius potentially benefits from a strategic advantage regionally in stimulating a relatively early economic recovery.

Expert views

April 20, 2020

Mauritius potentially benefits from a strategic advantage regionally in stimulating a relatively early economic recovery.

Expert views

April 17, 2020

Impact of COVID-19 on Mauritian Economy

Expert views

April 17, 2020

Impact of COVID-19 on Mauritian Economy

Expert views

March 13, 2020

Weekly Market Update as at 13 March 2020

Expert views

March 13, 2020

Weekly Market Update as at 13 March 2020

Expert views

March 09, 2020

“Gender equality creates the conditions to boost economic development and contributes to economic development”

Expert views

March 09, 2020

“Gender equality creates the conditions to boost economic development and contributes to economic development”

Expert views

February 12, 2020

“Brexit and coronavirus will necessarily have an impact on major currencies”

Expert views

February 12, 2020

“Brexit and coronavirus will necessarily have an impact on major currencies”

Business & Innovation

February 04, 2020

AfrAsia Bank wins for the third year in a row the Best Bank in Mauritius award

Business & Innovation

February 04, 2020

AfrAsia Bank wins for the third year in a row the Best Bank in Mauritius award

Expert views

January 17, 2020

"The contribution of the banking industry and its growth in the financial services sector has been phenomenal"

Expert views

January 17, 2020

"The contribution of the banking industry and its growth in the financial services sector has been phenomenal"

Differentiate. Inspire. Celebrate

January 07, 2020

AfrAsia Achiever Awards (AAA)

Differentiate. Inspire. Celebrate

January 07, 2020

AfrAsia Achiever Awards (AAA)

Golf

December 08, 2019

Danish teenager wins AfrAsia Bank Mauritius Open in playoff

Golf

December 08, 2019

Danish teenager wins AfrAsia Bank Mauritius Open in playoff

Golf

December 08, 2019

18-year-old claims dream win at AfrAsia Bank Mauritius Open in a playoff

Golf

December 08, 2019

18-year-old claims dream win at AfrAsia Bank Mauritius Open in a playoff

Golf

December 07, 2019

Rozner leads French charge in AfrAsia Bank Mauritius Open

Golf

December 07, 2019

Rozner leads French charge in AfrAsia Bank Mauritius Open

Golf

December 06, 2019

French golfers poised for historic win in AfrAsia Bank Mauritius Open

Golf

December 06, 2019

French golfers poised for historic win in AfrAsia Bank Mauritius Open

Golf

December 05, 2019

Relaxed Stone shares lead in AfrAsia Bank Mauritius Open

Golf

December 05, 2019

Relaxed Stone shares lead in AfrAsia Bank Mauritius Open

Golf

December 03, 2019

‘The most beautiful week in golf’ has top players talking

Golf

December 03, 2019

‘The most beautiful week in golf’ has top players talking

Testimonials

December 01, 2019

“With the world “slowing down” other jurisdictions are trying hard to challenge us.”

Testimonials

December 01, 2019

“With the world “slowing down” other jurisdictions are trying hard to challenge us.”

Business & Innovation

November 30, 2019

''Firms offering wealth services need to continue enhancing the client experience''

Business & Innovation

November 30, 2019

''Firms offering wealth services need to continue enhancing the client experience''

Testimonials

November 30, 2019

“We are treated not as customers but as partners”

Testimonials

November 30, 2019

“We are treated not as customers but as partners”

Golf

November 25, 2019

Coetzee, Harding, Stone join AfrAsia Bank Mauritius Open field

Golf

November 25, 2019

Coetzee, Harding, Stone join AfrAsia Bank Mauritius Open field

Business & Innovation

October 31, 2019

AfrAsia Bank bags two more prestigious international awards

Business & Innovation

October 31, 2019

AfrAsia Bank bags two more prestigious international awards

Testimonials

September 30, 2019

“This is really a different Bank where the customer’s well-being matters.”

Testimonials

September 30, 2019

“This is really a different Bank where the customer’s well-being matters.”

Testimonials

September 29, 2019

Differentiate. Inspire. Celebrate.

Testimonials

September 29, 2019

Differentiate. Inspire. Celebrate.

Expert views

September 28, 2019

"Throughout its history, Mauritius has always been able to re-invent itself in times of hardship."

Expert views

September 28, 2019

"Throughout its history, Mauritius has always been able to re-invent itself in times of hardship."

Expert views

September 20, 2019

"Africa is the hinterland for the Mauritian financial services space"

Expert views

September 20, 2019

"Africa is the hinterland for the Mauritian financial services space"

Expert views

June 14, 2019

What’s next for Private Wealth?

Expert views

June 14, 2019

What’s next for Private Wealth?

Expert views

April 24, 2019

"We provide connectivity to HNW South Africans investing offshore"

Expert views

April 24, 2019

"We provide connectivity to HNW South Africans investing offshore"

Expert views

April 23, 2019

Thierry Vallet, General Manager, speaks with Mauritius Golf Tours in an exclusive interview

Expert views

April 23, 2019

Thierry Vallet, General Manager, speaks with Mauritius Golf Tours in an exclusive interview

Business & Innovation

April 02, 2019

AfrAsia Bank recognised as a pioneer in the Digital HR Space by Oracle

Business & Innovation

April 02, 2019

AfrAsia Bank recognised as a pioneer in the Digital HR Space by Oracle

Expert views

March 15, 2019

There is clear visibility towards meaningful growth.

Expert views

March 15, 2019

There is clear visibility towards meaningful growth.

Testimonials

March 07, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE by Weekly

Testimonials

March 07, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE by Weekly

Testimonials

March 06, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE

Testimonials

March 06, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE

Expert views

January 22, 2019

Africa will play a major role in the commercial use of financial technology.

Expert views

January 22, 2019

Africa will play a major role in the commercial use of financial technology.

Testimonials

December 13, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

December 13, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

December 12, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Testimonials

December 12, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Business & Innovation

December 07, 2018

AfrAsia Bank wins 4 awards at the EMEA Finance’s African Banking Awards 2018

Business & Innovation

December 07, 2018

AfrAsia Bank wins 4 awards at the EMEA Finance’s African Banking Awards 2018

Golf

December 05, 2018

AfrAsia Bank Mastercard Pro-Am Results

Golf

December 05, 2018

AfrAsia Bank Mastercard Pro-Am Results

Golf

December 02, 2018

Kurt kicks on with breakthrough win in AfrAsia Bank Mauritius Open

Golf

December 02, 2018

Kurt kicks on with breakthrough win in AfrAsia Bank Mauritius Open

Golf

December 01, 2018

SA's Harding chasing win number five in Mauritius

Golf

December 01, 2018

SA's Harding chasing win number five in Mauritius

Golf

November 29, 2018

Els hoping local knowledge gives him the edge in Mauritius

Golf

November 29, 2018

Els hoping local knowledge gives him the edge in Mauritius

Testimonials

October 18, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

October 18, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

October 17, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Testimonials

October 17, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Expert views

October 10, 2018

“An ageing population is also synonymous to declining growth”

Expert views

October 10, 2018

“An ageing population is also synonymous to declining growth”

Expert views

September 28, 2018

Weekly Market Update as at 28 September 2018

Expert views

September 28, 2018

Weekly Market Update as at 28 September 2018

Expert views

September 26, 2018

Sustainability development is an essential condition to become a high-income country

Expert views

September 26, 2018

Sustainability development is an essential condition to become a high-income country

Expert views

September 21, 2018

Weekly Market Update as at 21 September 2018

Expert views

September 21, 2018

Weekly Market Update as at 21 September 2018

Expert views

September 07, 2018

Weekly Market Update as at 07 September 2018

Expert views

September 07, 2018

Weekly Market Update as at 07 September 2018

Expert views

August 31, 2018

Weekly Market Update as at 08 February 2019

Expert views

August 31, 2018

Weekly Market Update as at 08 February 2019

Expert views

August 31, 2018

Weekly Market Update as at 31 August 2018

Expert views

August 31, 2018

Weekly Market Update as at 31 August 2018

Expert views

August 24, 2018

Weekly Market Update as at 24 August 2018

Expert views

August 24, 2018

Weekly Market Update as at 24 August 2018

Expert views

August 17, 2018

Weekly Market Update as at 17 August 2018

Expert views

August 17, 2018

Weekly Market Update as at 17 August 2018

Expert views

August 03, 2018

Weekly Market Update as at 03 August 2018

Expert views

August 03, 2018

Weekly Market Update as at 03 August 2018

Expert views

July 27, 2018

Weekly Market Update as at 27 July 2018

Expert views

July 27, 2018

Weekly Market Update as at 27 July 2018

Golf

July 21, 2018

Gary Todd bags Pro-Am ticket to the AfrAsia Bank Mauritius Open 2018.

Golf

July 21, 2018

Gary Todd bags Pro-Am ticket to the AfrAsia Bank Mauritius Open 2018.

Expert views

July 17, 2018

Sanjiv Bhasin on Global Business sector: “A new market will open up”

Expert views

July 17, 2018

Sanjiv Bhasin on Global Business sector: “A new market will open up”

Expert views

July 06, 2018

Weekly Market Update as at 06 July 2018

Expert views

July 06, 2018

Weekly Market Update as at 06 July 2018

Golf

June 30, 2018

A spectacular kick-off round for a Pro-Am ticket at the AfrAsia Bank Mauritius Open 2018 at Anahita

Golf

June 30, 2018

A spectacular kick-off round for a Pro-Am ticket at the AfrAsia Bank Mauritius Open 2018 at Anahita

Expert views

June 29, 2018

Weekly Market Update as at 29 June 2018

Expert views

June 29, 2018

Weekly Market Update as at 29 June 2018

Expert views

June 22, 2018

Weekly Market Update on Radio One as at 22 June 2018

Expert views

June 22, 2018

Weekly Market Update on Radio One as at 22 June 2018

Expert views

June 13, 2018

"Mauritius is considered as one of the most stable countries in Africa"

Expert views

June 13, 2018

"Mauritius is considered as one of the most stable countries in Africa"

Expert views

June 12, 2018

Rethinking private banking

Expert views

June 12, 2018

Rethinking private banking

Golf

June 04, 2018

Sanjiv Bhasin, CEO, speaks with Mauritius Golf Tours in an exclusive interview

Golf

June 04, 2018

Sanjiv Bhasin, CEO, speaks with Mauritius Golf Tours in an exclusive interview

Business & Innovation

May 17, 2018

AfrAsia wins the Best Corporate Bank 2018 award for the second year in a row

Business & Innovation

May 17, 2018

AfrAsia wins the Best Corporate Bank 2018 award for the second year in a row

Expert views

May 15, 2018

'Mauritius has the benefit of being in Africa without being in mainland', says Assad Abdullatiff

Expert views

May 15, 2018

'Mauritius has the benefit of being in Africa without being in mainland', says Assad Abdullatiff

Expert views

May 15, 2018

IFRS9 - What you need to know by Robin Smither

Expert views

May 15, 2018

IFRS9 - What you need to know by Robin Smither

Business & Innovation

May 15, 2018

Banking on customer centricity

Business & Innovation

May 15, 2018

Banking on customer centricity

Community

May 15, 2018

Supporting the communities where we live and work

Community

May 15, 2018

Supporting the communities where we live and work

Events & Webinar

May 15, 2018

AfrAsia Bank Roadshow: Johannesburg business elites under one roof

Events & Webinar

May 15, 2018

AfrAsia Bank Roadshow: Johannesburg business elites under one roof

Events & Webinar

May 15, 2018

AfrAsia Bank Real Estate Seminar: The property investment hotspots revealed

Events & Webinar

May 15, 2018

AfrAsia Bank Real Estate Seminar: The property investment hotspots revealed

Events & Webinar

May 14, 2018

AfrAsia & SA Chamber of Commerce host futurist expert, Anton Musgrave for thought-provoking experience

Events & Webinar

May 14, 2018

AfrAsia & SA Chamber of Commerce host futurist expert, Anton Musgrave for thought-provoking experience

Business & Innovation

January 01, 0001

A clientele made up of 70% foreigners

Business & Innovation

January 01, 0001

A clientele made up of 70% foreigners