Mauritius is back in business – What to expect for the Tourism/Hospitality and Real Estate sectors?

Published on

November 22, 2021

Published in Category

Expert views

After nearly 18 months of navigating through 2 national lockdowns, stern sanitary restrictions, and a national border shutdown, Mauritius revived its international travel on 1st October 2021. Boasting one of the strongest African economies, Mauritius has had to paddle its own canoe as best as possible to navigate through the storm. Now that it’s back in business, what can the Island, significantly reliant on the tourism and hospitality sectors, expect for the upcoming weeks, months and year even? Rajeev Basgeet – Partner at PwC, Anusha Ramkhalawon – Senior Relationship Manager at AfrAsia, and Suunil Goreeba – Senior Relationship Manager at AfrAsia unpack the opportunities and challenges ahead for the real estate and hospitality sectors.

With the reopening of our international borders, how do you foresee the business arena to evolve over the next one year or so?

Rajeev Basgeet: A sense of normalcy, or rather “new normalcy” is expected to gradually sink in. I say this with some caution considering that COVID-19 is not yet behind us. Following the vaccination roll-out in Mauritius and with the country out of the FATF Grey List, the timing could not have been more opportune. Given that both the financial and hospitality sectors are two major contributors to our GDP, these events represent a significant boost for our economic recovery. An improvement in these two business activities, coupled with a manufacturing sector that has held well – availing of currency movements – are solid grounds for optimism for the business climate to improve over the next year or so. Business activities related to these economic segments such as Real Estate and SMEs, amongst others, should also experience some much-needed recovery.

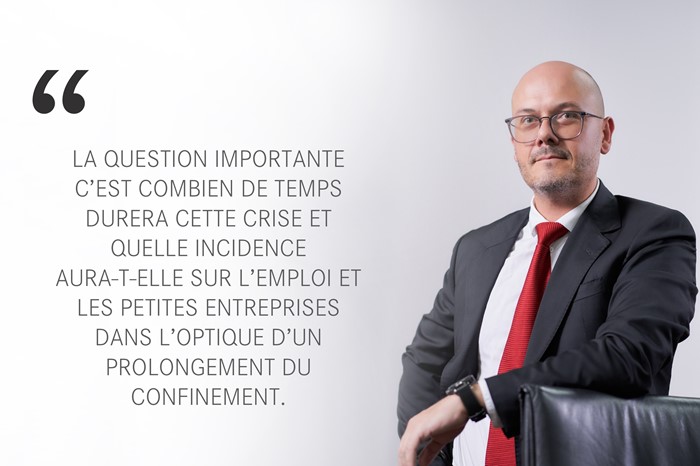

That said, we are not to overlook the challenges that await us in rebooting the economy in a sustainable fashion. One key challenge is likely to be the delivery delays birthed by global disruptions in supply chains which will eventually impact consumerism. Another pointer to consider is the productivity element of our workforce. These could have a significant bearing on our recovery, especially in the manufacturing and hospitality sectors. Therefore, such dynamics have to be managed carefully.

What I am discussing are the pillars of our “old” economy. With the business environment expected to improve, our agenda should be to build the foundations of a “New Economy” by standing strong and together to buttress our resilience to any future shocks and regain our competitive advantage. Here, both the public and private sectors should work together to explore the potential of underexploited arenas such as the Blue Economy and/or even develop a new business model for the economy anchored on sustainable goals. Complementing our collective efforts with trust and faith in our own abilities as well as a skilled workforce, we will eventually get Mauritius back on track. True it is to say that we should not underestimate the variants of COVID-19, especially with the emergence of the Delta variant on our territory. That said, other than forging ahead together with confidence, we’ve got no other choice.

How is the changing macroeconomic landscape likely to impact the banking and financial sector?

Anusha Ramkhalawon: The Mauritian economy has entered its new normal, so there is no question of going back to the old one at all. Private sector debt, which includes both corporate and household debt, is comfortably above 92% of this year’s projected GDP while public sector debt is marginally higher. With such elevated debt levels, especially when compared to public sector revenues - including unfunded liabilities and relative to free cash flows for the non-financial private sector - the growth outlook remains moderate at best, given our positioning across the debt cycle. Gross national savings also stands at around 8% of GDP which will make attracting more foreign direct investments key when it comes to stimulating overall investments.

While moratoriums and state support in terms of MIC (Mauritius Investment Corporation) bailouts and in terms of wage assistance schemes have helped to prevent the worst in terms of defaults, many sectors such as the hospitality have seen little bar a few exceptions in terms of recapitalisation and industry consolidation (mergers and acquisition activity). The key for Mauritius to eventually get back to a sustainable low-to-mid 3% growth path over the medium term revolves around the ability of both the private and public sectors to successfully navigate the deleveraging process to come.

Given high-debt to free-cash flow levels across certain sectors of the economy, we anticipate that banks are likely to remain more conservative and focus more on quality in sectors such as health care which have more defensive qualities and also benefit from long-term structural trends such as our ageing demographics. With the motto of the forthcoming decade likely to revolve around revamping old business models and balance sheet cleansing, we expect that more flexible forms of financing across the capital structure to gain increasing traction from credit lenders via increased customised credit issuance: structured notes, convertible bonds and the like.

If we look at the hospitality industry, specifically the tourism sector, in light of the recent support measures provided by the Government to help its revival, what kind of recovery and growth are we likely to witness?

Suunil Goreeba: The Mauritian economy is reliant on the tourism sector as it contributes directly and indirectly to around 25% of the GDP and accounts for 20% of total employment. In order to provide the required support to this sector, the Government implemented two key measures:

- Long-term funding to operators in this sector through MIC’s 9-year convertible preference bonds to be used to finance working capital requirements during these challenging times;

- Government Wage Assistance Scheme (GWAS) which is a wage subsidy to employers, as a response to Covid-19, to ensure that all employees are duly paid their salaries;

The minister of finance also confirmed that the authorities shall come forth with measures to support the tourism industry, in the event of lower-than-forecasted arrivals post the reopening of borders.

Mauritius has been welcoming international visitors since the middle of July and the “in resort bubbles” strategy has allowed some resorts on the Island to resume their activities albeit with a low occupancy rate. However, with the full re-opening of borders to vaccinated tourists since beginning of October, the main operators in the tourism sector have confirmed an occupancy rate of above 50% for this 10th month of the year. A total of 54,000 tourists visited the Island for the during October 2021, with nearly 80% of them coming from Europe. This is a very encouraging trend for this sector. The industry is expecting an occupancy rate above 60% for the months of November and December 2021 provided there are no changes to international travel norms and availability of air seats. The country is able to retain its high-end tourists as the 5-star resort cluster is currently ahead of the lower star peers in terms of occupancy.

The latter is coupled to the fact that on the air connection side, since October, an additional five airlines are operating a connection to Mauritius (Air Seychelles, Austrian Airlines, Corsair Airline, Condor Airline and Air Belgium). The 120,000 passenger arrivals forecasted for November looks promising. Jocelyn Kwok, CEO of AHRIM (The hotels & restaurant association of Mauritius) is optimistic with regards to the average occupancy rates for the hoteliers in November and December to fare better than the anticipated 50% & 65% respectively. The country is able to retain its high-end tourists as the 5-star resort cluster is currently ahead of the lower star peers in terms of occupancy according to him.

The Government has been working on different scenarios regarding tourist arrivals, with a base case seeing approximately 300,000 arrivals in 2021 and 650,000 arrivals for the period ended June 2022. So, this gives us hope that this sector will pick up gradually and can reach pre-COVID occupancy levels by 2023. This also means that auxiliary industries are likely to also pick up. Here, I am referring, amongst others, to the food and beverages sector, the agricultural production and even the real estate sector to a certain extent.

Speaking of the Mauritian real estate sector, how is it faring at the moment and how bright is the future ahead?

Anusha Ramkhalawon: Global financial conditions remain easy with real estate markets globally benefiting from significant liquidity. Rising inflation pressures globally when coupled with increased talk of Fed Reserve tapering however may moderate optimism on this front. When it comes to the local higher-end real estate markets, prices are not likely to experience any major fluctuations which will prompt those to be resilient in the short term. We do continue to see opportunities in the Smart and Green integrated real estate projects which target retirees and the future definitely looks bright here, to say the least! Nevertheless, we remain cautious, and maybe even less optimistic, with regards to high-end villa sales over the medium term.

Rajeev Basgeet: If you’d recall, even before the pandemic struck, there was a sense of nervousness that the economy was overly exposed to the property sector. There was also discussion around a potential bubble that may burst. Credit origination towards this sector was under enhanced supervision.

With COVID-19, demand may have dampened, but the confidence level in the sector appears to be holding strong. And, that’s positive. Lately, we have noted major development projects being planned. Developers have remodelled or adapted their projects to take into account the evolving aspirations of buyers. New projects are factoring in the notion of smart and green concepts to improve the lifestyle experiences of future buyers. A new wave of demand is likely to flow into these segments that is likely to keep the real estate sector thriving.

The challenge, as we see it for developers, could be about finding the right trade-off for past projects yet to be sold, whilst managing the changing aspirations of buyers. We need to watch out for delays in project delivery which may dampen confidence. As we note globally, government support towards distressed real estate projects is not forthcoming. Credit flow into the sector is essential to sustain the sector both from a supply and demand perspective.

The Government has also put forward schemes over the years to assist non-residents to own property in Mauritius. This has been further reinforced by the proposed 2021-2022 budgetary measures over the past couple of years, including the ‘Premium Visa’ scheme, the extension of maximum duration for Occupation Permits for foreign professionals from 3 to 10 years and Permanent Residency Permits from 10 to 20 years as well as a reduction from USD 500k to USD 375k to own a villa in Mauritius.

That said, although we have important players that should be able to keep the sector strong, we should continue to challenge ourselves to see how the property clusters can continue to sustainably drive future GDP growth.

Is it the right time to invest in real estate?

Rajeev Basgeet: At a macroscopic level, a degree of optimism is back, and investors are gaining in confidence. So, there could be an opportunity that may cater for all segments: be it High Net Worth (HNW) individuals, residents or non-residents. Supply side is not constrained. With continued credit availability, it may well represent an investment opportunity. To get this right, it’s now time to market these opportunities as part of the hospitality sector global campaigns, and for banks with a strong HNW or private banking clientele to showcase these investment opportunities. For example, a technology platform could be considered on how best to connect all these players (developers, banks, and buyers) to speed up the investment process.

Anusha Ramkhalawon: In view of the increasing public debt on a global scale, western tax authorities will be under increased pressure to close taxation gaps which benefit the rich. Offshore jurisdictions are more likely than not to face more challenges than they did in the past, including in real estate where foreigners benefited from tax savings from being residents. However, with the cost of living everywhere rising and baby boomers retiring, should Mauritius be able to offer a competitive product when it comes to retirement living along with associated facilities such as better and higher quality private health care and long-term care, this real estate segment is likely to attract foreign investments and retiree demand. Couple this to the fact that Mauritius is now out of the FATF Grey List and all stakeholders are at work to reinforce its positioning as an International Financial Centre of substance, we can say that we can surely see the beaming light at the end of the tunnel.

Should you wish to know more from our experts, get in touch with us at afrasia@afrasiabank.com

Expert views

May 26, 2026

AfrAsia wants to be the Premier Bridge between Global Capital and African Opportunity

Expert views

May 26, 2026

AfrAsia wants to be the Premier Bridge between Global Capital and African Opportunity

Expert views

May 06, 2026

A Strategic Window in a Volatile World

Expert views

May 06, 2026

A Strategic Window in a Volatile World

Expert views

January 20, 2026

What is the right investment strategy for you?

Expert views

January 20, 2026

What is the right investment strategy for you?

Expert views

October 22, 2025

Mauritius–UAE: A Strategic Bridge to Africa

Expert views

October 22, 2025

Mauritius–UAE: A Strategic Bridge to Africa

Expert views

August 14, 2024

Mauritius as a gateway for investment and transfer of capacity to Africa.

Expert views

August 14, 2024

Mauritius as a gateway for investment and transfer of capacity to Africa.

Expert views

July 26, 2024

We have seen a marked increase in initiatives aimed at supporting women’s entry and advancement in the finance industry.

Expert views

July 26, 2024

We have seen a marked increase in initiatives aimed at supporting women’s entry and advancement in the finance industry.

Expert views

June 11, 2024

With Africa’s projected continued growth, a robust banking network is crucial.

Expert views

June 11, 2024

With Africa’s projected continued growth, a robust banking network is crucial.

Expert views

March 15, 2024

Tailored Financial Excellence: Mauritius’ Unique Investor Advantages

Expert views

March 15, 2024

Tailored Financial Excellence: Mauritius’ Unique Investor Advantages

Expert views

May 11, 2023

Banking on sustainable finance to scale up the Mauritius IFC

Expert views

May 11, 2023

Banking on sustainable finance to scale up the Mauritius IFC

Expert views

May 10, 2023

Mauritius & South Africa: A mutually beneficial trade relationship

Expert views

May 10, 2023

Mauritius & South Africa: A mutually beneficial trade relationship

Expert views

April 17, 2023

Mauritius IFC: From a conventional jurisdiction to a forward-looking hub

Expert views

April 17, 2023

Mauritius IFC: From a conventional jurisdiction to a forward-looking hub

Golf

December 18, 2022

Record win for Rozner in AfrAsia Bank Mauritius Open

Golf

December 18, 2022

Record win for Rozner in AfrAsia Bank Mauritius Open

Golf

December 17, 2022

Rozner chasing AfrAsia Bank Mauritius Open glory

Golf

December 17, 2022

Rozner chasing AfrAsia Bank Mauritius Open glory

Golf

December 16, 2022

Rozner in the hunt again at AfrAsia Bank Mauritius Open

Golf

December 16, 2022

Rozner in the hunt again at AfrAsia Bank Mauritius Open

Golf

December 15, 2022

Course record for Välimäki to lead AfrAsia Bank Mauritius Open

Golf

December 15, 2022

Course record for Välimäki to lead AfrAsia Bank Mauritius Open

Expert views

December 01, 2022

Africa’s Drive Towards Sustainability: Launch of ESG GPS in Mauritius

Expert views

December 01, 2022

Africa’s Drive Towards Sustainability: Launch of ESG GPS in Mauritius

Expert views

October 20, 2022

Quelle est l'influence des taux d'intérêt sur le prix de l'or?

Expert views

October 20, 2022

Quelle est l'influence des taux d'intérêt sur le prix de l'or?

Golf

October 18, 2022

Mont Choisy Le Golf set to impress as host of 2022 AfrAsia Bank Mauritius Open

Golf

October 18, 2022

Mont Choisy Le Golf set to impress as host of 2022 AfrAsia Bank Mauritius Open

Golf

September 16, 2022

Burmester confirmed for 2022 AfrAsia Bank Mauritius Open

Golf

September 16, 2022

Burmester confirmed for 2022 AfrAsia Bank Mauritius Open

Expert views

July 28, 2022

EUR/USD – la roupie prise en étau

Expert views

July 28, 2022

EUR/USD – la roupie prise en étau

Expert views

June 01, 2022

Africa CEO Forum 2022 - Malachy McAllister on CNBC Africa

Expert views

June 01, 2022

Africa CEO Forum 2022 - Malachy McAllister on CNBC Africa

Differentiate. Inspire. Celebrate

April 29, 2022

AfrAsia Bank further sharpens its expertise with Elliott Wave Certification

Differentiate. Inspire. Celebrate

April 29, 2022

AfrAsia Bank further sharpens its expertise with Elliott Wave Certification

Expert views

March 04, 2022

Journée des droits des femmes: STOP aux freins invisibles

Expert views

March 04, 2022

Journée des droits des femmes: STOP aux freins invisibles

Expert views

March 04, 2022

The real opportunity and uniqueness of Mauritius lies in its diversified economic landscape with opportunities in various sectors.

Expert views

March 04, 2022

The real opportunity and uniqueness of Mauritius lies in its diversified economic landscape with opportunities in various sectors.

Expert views

March 02, 2022

La crise Russie-Ukraine : Quels sont les enjeux financiers à prévoir ?

Expert views

March 02, 2022

La crise Russie-Ukraine : Quels sont les enjeux financiers à prévoir ?

Testimonials

February 08, 2022

'AfrAsia Bank has always been a trusted financial partner for us.'

Testimonials

February 08, 2022

'AfrAsia Bank has always been a trusted financial partner for us.'

Testimonials

February 08, 2022

“ Their legacy-building ethos and customer service structure resonates with us.”

Testimonials

February 08, 2022

“ Their legacy-building ethos and customer service structure resonates with us.”

Expert views

January 19, 2022

Preserving the human touch in banking in the digital age

Expert views

January 19, 2022

Preserving the human touch in banking in the digital age

Expert views

November 22, 2021

A new era for the Mauritius IFC

Expert views

November 22, 2021

A new era for the Mauritius IFC

Expert views

November 22, 2021

A Purposeful Brand - It's not about 'I', it's about 'We'

Expert views

November 22, 2021

A Purposeful Brand - It's not about 'I', it's about 'We'

Expert views

November 03, 2021

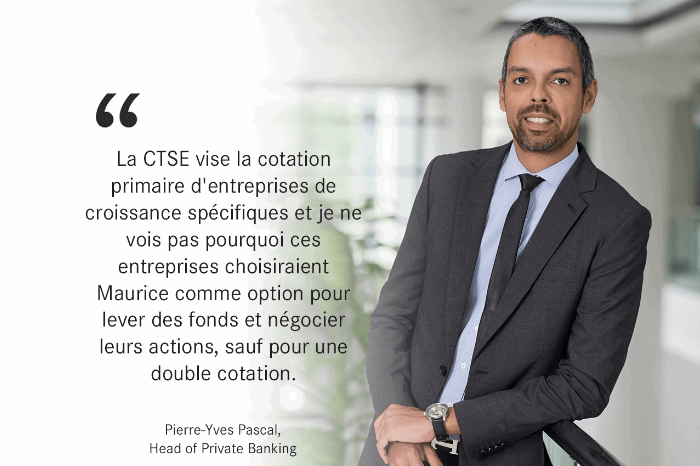

Quels sont les enjeux pour la Bourse de Maurice avec l’arrivée du Cape Town Stock Exchange ?

Expert views

November 03, 2021

Quels sont les enjeux pour la Bourse de Maurice avec l’arrivée du Cape Town Stock Exchange ?

Expert views

October 20, 2021

#Stagflation : Comment s’adapter à cet nouvel ordre économique ?

Expert views

October 20, 2021

#Stagflation : Comment s’adapter à cet nouvel ordre économique ?

Expert views

October 20, 2021

Fonds d’investissements : Est-ce le moment d’investir ?

Expert views

October 20, 2021

Fonds d’investissements : Est-ce le moment d’investir ?

Expert views

October 18, 2021

Marché des changes: Quel est l’impact sur nos réserves en devises étrangères ?

Expert views

October 18, 2021

Marché des changes: Quel est l’impact sur nos réserves en devises étrangères ?

Expert views

September 15, 2021

« Le marché de la banque privée est amené a plus que doubler au cours des cinq prochaines années »

Expert views

September 15, 2021

« Le marché de la banque privée est amené a plus que doubler au cours des cinq prochaines années »

Expert views

September 01, 2021

Rather than a purely government or business matter, country branding is more of a concerted and integrated effort made by all stakeholders, including the population.

Expert views

September 01, 2021

Rather than a purely government or business matter, country branding is more of a concerted and integrated effort made by all stakeholders, including the population.

Expert views

August 11, 2021

More activities expected between India and Africa via Mauritius

Expert views

August 11, 2021

More activities expected between India and Africa via Mauritius

Expert views

August 04, 2021

Repo Rate à 1.85% - Maintenir la tendance baissière des 5 dernières années ou pas ?

Expert views

August 04, 2021

Repo Rate à 1.85% - Maintenir la tendance baissière des 5 dernières années ou pas ?

Expert views

August 01, 2021

What is a Structured Product?

Expert views

August 01, 2021

What is a Structured Product?

Expert views

July 14, 2021

Global Battery Market powered by Automotive Electrification - Structured Product

Expert views

July 14, 2021

Global Battery Market powered by Automotive Electrification - Structured Product

Expert views

July 13, 2021

Deepening our Expertise to serve you better

Expert views

July 13, 2021

Deepening our Expertise to serve you better

Expert views

July 12, 2021

Meet our new Head of Sustainability and CSR, Alvin Peerthy

Expert views

July 12, 2021

Meet our new Head of Sustainability and CSR, Alvin Peerthy

Expert views

July 05, 2021

The Mauritian Rupee faces the COVID-19 brunt

Expert views

July 05, 2021

The Mauritian Rupee faces the COVID-19 brunt

Events & Webinar

June 30, 2021

#Webinar Replay: Cross-border opportunities and challenges in Africa

Events & Webinar

June 30, 2021

#Webinar Replay: Cross-border opportunities and challenges in Africa

Events & Webinar

June 14, 2021

20 Min with AfrAsia Webinar - Digital Transformation to build a Sustainable Business

Events & Webinar

June 14, 2021

20 Min with AfrAsia Webinar - Digital Transformation to build a Sustainable Business

Expert views

June 09, 2021

Millionaires in Africa: an attractive market for Mauritius

Expert views

June 09, 2021

Millionaires in Africa: an attractive market for Mauritius

Expert views

June 07, 2021

La charge est-elle équitablement partagée entre l’Étate et le privé?

Expert views

June 07, 2021

La charge est-elle équitablement partagée entre l’Étate et le privé?

Expert views

May 26, 2021

The revival of the UK-Mauritius trade together with the tourism sector could generate more revenue and appreciate the Mauritian rupee

Expert views

May 26, 2021

The revival of the UK-Mauritius trade together with the tourism sector could generate more revenue and appreciate the Mauritian rupee

Expert views

May 21, 2021

Tant que nos frontières restent fermées, cette pénurie devrait se poursuivre dans le proche avenir.

Expert views

May 21, 2021

Tant que nos frontières restent fermées, cette pénurie devrait se poursuivre dans le proche avenir.

Events & Webinar

May 21, 2021

Retour sur notre #webinaire : Gestion de patrimoine - Post COVID

Events & Webinar

May 21, 2021

Retour sur notre #webinaire : Gestion de patrimoine - Post COVID

Expert views

May 19, 2021

Local customers represent 70% of these assets.

Expert views

May 19, 2021

Local customers represent 70% of these assets.

Expert views

May 13, 2021

Global vaccination campaign, Inflation and Financial Assets – let’s talk!

Expert views

May 13, 2021

Global vaccination campaign, Inflation and Financial Assets – let’s talk!

Expert views

May 12, 2021

Automotive Electrification and the Global Battery Market – are Nickel, Copper and Aluminium your next investment opportunity?

Expert views

May 12, 2021

Automotive Electrification and the Global Battery Market – are Nickel, Copper and Aluminium your next investment opportunity?

Expert views

May 11, 2021

Cybersecurity Awakening

Expert views

May 11, 2021

Cybersecurity Awakening

Events & Webinar

April 07, 2021

How Mauritius remains a relevant IFC for South African Corporates & Individuals?

Events & Webinar

April 07, 2021

How Mauritius remains a relevant IFC for South African Corporates & Individuals?

Expert views

March 24, 2021

Marc-Alexandre Masnin, Directeur des investissements - Business Magazine

Expert views

March 24, 2021

Marc-Alexandre Masnin, Directeur des investissements - Business Magazine

Expert views

March 24, 2021

At the height of the crisis last year, the price of the oil barrel turned negative. However, it hovers today above 60 dollars. Is this a show of confidence in a faster economic recovery?

Expert views

March 24, 2021

At the height of the crisis last year, the price of the oil barrel turned negative. However, it hovers today above 60 dollars. Is this a show of confidence in a faster economic recovery?

Community

March 18, 2021

#InternationalWomensDay: Do you Choose to Challenge?

Community

March 18, 2021

#InternationalWomensDay: Do you Choose to Challenge?

Expert views

March 17, 2021

L’économie mauricienne peut-elle survivre à un deuxième confinement ?

Expert views

March 17, 2021

L’économie mauricienne peut-elle survivre à un deuxième confinement ?

Community

March 08, 2021

#InternationalWomensDay: Do you Choose to Challenge?

Community

March 08, 2021

#InternationalWomensDay: Do you Choose to Challenge?

The Believers in Local

February 16, 2021

#AfrAsiaBankLocalMarket – Chinese New Year & Valentine’s Day

The Believers in Local

February 16, 2021

#AfrAsiaBankLocalMarket – Chinese New Year & Valentine’s Day

Expert views

February 11, 2021

Interview with Robin Smither, Senior Executive, Head of Corporate Banking, AfrAsia Bank

Expert views

February 11, 2021

Interview with Robin Smither, Senior Executive, Head of Corporate Banking, AfrAsia Bank

Expert views

February 03, 2021

Jolene Li Sing How, one of the very first Certified Elliott Wave Analysts

Expert views

February 03, 2021

Jolene Li Sing How, one of the very first Certified Elliott Wave Analysts

Expert views

January 20, 2021

AfrAsia was awarded two distinctions by Elliott Wave International.

Expert views

January 20, 2021

AfrAsia was awarded two distinctions by Elliott Wave International.

The Believers in Local

December 23, 2020

The believers in local - Christmas Market

The Believers in Local

December 23, 2020

The believers in local - Christmas Market

Expert views

December 16, 2020

Mauritius on the EU Black List, what impact since October 1st, 2020?

Expert views

December 16, 2020

Mauritius on the EU Black List, what impact since October 1st, 2020?

Expert views

December 14, 2020

Marché des cartes – la dématérialisation enclenchée

Expert views

December 14, 2020

Marché des cartes – la dématérialisation enclenchée

Events & Webinar

December 09, 2020

How does Mauritius remain a relevant International Financial Centre for South African corporates and individuals?

Events & Webinar

December 09, 2020

How does Mauritius remain a relevant International Financial Centre for South African corporates and individuals?

Expert views

November 18, 2020

«Face aux incertitudes actuelles, privilégier une approche core-satellite»

Expert views

November 18, 2020

«Face aux incertitudes actuelles, privilégier une approche core-satellite»

Expert views

November 18, 2020

Nantes Lavin interview on Business Mag

Expert views

November 18, 2020

Nantes Lavin interview on Business Mag

Expert views

October 29, 2020

ESG and Responsible Investments – Breaking through to shape a Sustainable World

Expert views

October 29, 2020

ESG and Responsible Investments – Breaking through to shape a Sustainable World

Expert views

October 28, 2020

Is Biden winning the forthcoming US Presidential Elections?

Expert views

October 28, 2020

Is Biden winning the forthcoming US Presidential Elections?

Expert views

October 27, 2020

Global Wealth Migration Review 2020

Expert views

October 27, 2020

Global Wealth Migration Review 2020

Differentiate. Inspire. Celebrate

October 26, 2020

Meet David Chamtyoo, our Elite Achiever of the Year 2019

Differentiate. Inspire. Celebrate

October 26, 2020

Meet David Chamtyoo, our Elite Achiever of the Year 2019

The Believers in Local

October 26, 2020

Our very first Local Market

The Believers in Local

October 26, 2020

Our very first Local Market

Expert views

October 21, 2020

The best international managers have lost money"

Expert views

October 21, 2020

The best international managers have lost money"

Expert views

October 14, 2020

Étant à ce jour «Covid-free», l’île Maurice jouit-elle d’un écosystème robuste pour assurer la protection de vos actifs?

Expert views

October 14, 2020

Étant à ce jour «Covid-free», l’île Maurice jouit-elle d’un écosystème robuste pour assurer la protection de vos actifs?

Events & Webinar

October 07, 2020

20 min with AfrAsia - Environment, Social & Governance (ESG) and Responsible Investments

Events & Webinar

October 07, 2020

20 min with AfrAsia - Environment, Social & Governance (ESG) and Responsible Investments

Expert views

September 30, 2020

The inclusion of Mauritius on the European Union's blacklist is a considerable hindrance to the image of our international financial center.

Expert views

September 30, 2020

The inclusion of Mauritius on the European Union's blacklist is a considerable hindrance to the image of our international financial center.

Events & Webinar

September 24, 2020

Webinar : Foreigners taking up Mauritian Tax Residency – Should they be worried about their Mauritian Trust?

Events & Webinar

September 24, 2020

Webinar : Foreigners taking up Mauritian Tax Residency – Should they be worried about their Mauritian Trust?

Expert views

September 21, 2020

Luvna Arnassalon-Seerungen: “Covid-19 has further put sustainability under the corporate spotlight”

Expert views

September 21, 2020

Luvna Arnassalon-Seerungen: “Covid-19 has further put sustainability under the corporate spotlight”

Expert views

September 17, 2020

Boosting Mauritius’ reputation as a key enabler of trade

Expert views

September 17, 2020

Boosting Mauritius’ reputation as a key enabler of trade

Business & Innovation

September 10, 2020

AfrAsia Customer Survey 2020

Business & Innovation

September 10, 2020

AfrAsia Customer Survey 2020

Expert views

September 08, 2020

Le Défi Quotidien : Marc-Alexandre Masnin, Head of Wealth Management- International / Investment Sales, AfrAsia Bank

Expert views

September 08, 2020

Le Défi Quotidien : Marc-Alexandre Masnin, Head of Wealth Management- International / Investment Sales, AfrAsia Bank

The Believers in Local

August 21, 2020

Believers in the passion of our entrepreneurs

The Believers in Local

August 21, 2020

Believers in the passion of our entrepreneurs

Expert views

August 19, 2020

Rakesh Seesurn, Head of Risk in Business Mag

Expert views

August 19, 2020

Rakesh Seesurn, Head of Risk in Business Mag

Expert views

August 18, 2020

Mauritius remains the best gateway for cross-border investments into Africa.

Expert views

August 18, 2020

Mauritius remains the best gateway for cross-border investments into Africa.

Events & Webinar

July 27, 2020

20 min with AfrAsia - Mauritius: More than just a property investment.

Events & Webinar

July 27, 2020

20 min with AfrAsia - Mauritius: More than just a property investment.

Expert views

July 01, 2020

Impacts of COVID-19 on South African Economy

Expert views

July 01, 2020

Impacts of COVID-19 on South African Economy

Expert views

July 01, 2020

Blue economy aims at generating multiple cash-flows from a portfolio of local opportunities

Expert views

July 01, 2020

Blue economy aims at generating multiple cash-flows from a portfolio of local opportunities

Community

July 01, 2020

Education remains key to success, even in a different normal

Community

July 01, 2020

Education remains key to success, even in a different normal

Expert views

June 29, 2020

EU blacklist: highly prejudicial to the economy

Expert views

June 29, 2020

EU blacklist: highly prejudicial to the economy

The Believers in Local

June 22, 2020

Believers in the authenticity of our talents

The Believers in Local

June 22, 2020

Believers in the authenticity of our talents

Expert views

June 08, 2020

As businesses undergo digital transformations in their front and back office operations, similarly cybercriminals are advancing the sophistication of their methods.

Expert views

June 08, 2020

As businesses undergo digital transformations in their front and back office operations, similarly cybercriminals are advancing the sophistication of their methods.

Expert views

June 06, 2020

The difference in taxation of foreign residents and Mauritian residents in the case of the Solidarity Levy is a first for the country

Expert views

June 06, 2020

The difference in taxation of foreign residents and Mauritian residents in the case of the Solidarity Levy is a first for the country

Community

June 01, 2020

Happy Mothers’ and Fathers’ Day!

Community

June 01, 2020

Happy Mothers’ and Fathers’ Day!

Expert views

May 21, 2020

Managing credit risks diligently

Expert views

May 21, 2020

Managing credit risks diligently

Expert views

May 21, 2020

In our opinion, the most impacted sector of the economy at this stage is the hospitality and tourism industry.

Expert views

May 21, 2020

In our opinion, the most impacted sector of the economy at this stage is the hospitality and tourism industry.

Expert views

May 20, 2020

A coordinated response to the impact of the crisis.

Expert views

May 20, 2020

A coordinated response to the impact of the crisis.

Expert views

May 08, 2020

COVID-19 - Operational Challenges v/s Technological Opportunities

Expert views

May 08, 2020

COVID-19 - Operational Challenges v/s Technological Opportunities

Expert views

May 07, 2020

“Converting the central bank into a magical money tree could lead to a significant currency devaluation”

Expert views

May 07, 2020

“Converting the central bank into a magical money tree could lead to a significant currency devaluation”

Expert views

May 06, 2020

“Banks will need to review their internal audit system”

Expert views

May 06, 2020

“Banks will need to review their internal audit system”

Expert views

April 27, 2020

Mastering market volatility is a key determinant for investors.

Expert views

April 27, 2020

Mastering market volatility is a key determinant for investors.

Expert views

April 22, 2020

Banks have a key role to play in economic recovery

Expert views

April 22, 2020

Banks have a key role to play in economic recovery

Expert views

April 20, 2020

Mauritius potentially benefits from a strategic advantage regionally in stimulating a relatively early economic recovery.

Expert views

April 20, 2020

Mauritius potentially benefits from a strategic advantage regionally in stimulating a relatively early economic recovery.

Expert views

April 17, 2020

Impact of COVID-19 on Mauritian Economy

Expert views

April 17, 2020

Impact of COVID-19 on Mauritian Economy

Expert views

March 13, 2020

Weekly Market Update as at 13 March 2020

Expert views

March 13, 2020

Weekly Market Update as at 13 March 2020

Expert views

March 09, 2020

“Gender equality creates the conditions to boost economic development and contributes to economic development”

Expert views

March 09, 2020

“Gender equality creates the conditions to boost economic development and contributes to economic development”

Expert views

February 12, 2020

“Brexit and coronavirus will necessarily have an impact on major currencies”

Expert views

February 12, 2020

“Brexit and coronavirus will necessarily have an impact on major currencies”

Business & Innovation

February 04, 2020

AfrAsia Bank wins for the third year in a row the Best Bank in Mauritius award

Business & Innovation

February 04, 2020

AfrAsia Bank wins for the third year in a row the Best Bank in Mauritius award

Expert views

January 17, 2020

"The contribution of the banking industry and its growth in the financial services sector has been phenomenal"

Expert views

January 17, 2020

"The contribution of the banking industry and its growth in the financial services sector has been phenomenal"

Differentiate. Inspire. Celebrate

January 07, 2020

AfrAsia Achiever Awards (AAA)

Differentiate. Inspire. Celebrate

January 07, 2020

AfrAsia Achiever Awards (AAA)

Golf

December 08, 2019

Danish teenager wins AfrAsia Bank Mauritius Open in playoff

Golf

December 08, 2019

Danish teenager wins AfrAsia Bank Mauritius Open in playoff

Golf

December 08, 2019

18-year-old claims dream win at AfrAsia Bank Mauritius Open in a playoff

Golf

December 08, 2019

18-year-old claims dream win at AfrAsia Bank Mauritius Open in a playoff

Golf

December 07, 2019

Rozner leads French charge in AfrAsia Bank Mauritius Open

Golf

December 07, 2019

Rozner leads French charge in AfrAsia Bank Mauritius Open

Golf

December 06, 2019

French golfers poised for historic win in AfrAsia Bank Mauritius Open

Golf

December 06, 2019

French golfers poised for historic win in AfrAsia Bank Mauritius Open

Golf

December 05, 2019

Relaxed Stone shares lead in AfrAsia Bank Mauritius Open

Golf

December 05, 2019

Relaxed Stone shares lead in AfrAsia Bank Mauritius Open

Golf

December 03, 2019

‘The most beautiful week in golf’ has top players talking

Golf

December 03, 2019

‘The most beautiful week in golf’ has top players talking

Testimonials

December 01, 2019

“With the world “slowing down” other jurisdictions are trying hard to challenge us.”

Testimonials

December 01, 2019

“With the world “slowing down” other jurisdictions are trying hard to challenge us.”

Business & Innovation

November 30, 2019

''Firms offering wealth services need to continue enhancing the client experience''

Business & Innovation

November 30, 2019

''Firms offering wealth services need to continue enhancing the client experience''

Testimonials

November 30, 2019

“We are treated not as customers but as partners”

Testimonials

November 30, 2019

“We are treated not as customers but as partners”

Golf

November 25, 2019

Coetzee, Harding, Stone join AfrAsia Bank Mauritius Open field

Golf

November 25, 2019

Coetzee, Harding, Stone join AfrAsia Bank Mauritius Open field

Business & Innovation

October 31, 2019

AfrAsia Bank bags two more prestigious international awards

Business & Innovation

October 31, 2019

AfrAsia Bank bags two more prestigious international awards

Testimonials

September 30, 2019

“This is really a different Bank where the customer’s well-being matters.”

Testimonials

September 30, 2019

“This is really a different Bank where the customer’s well-being matters.”

Testimonials

September 29, 2019

Differentiate. Inspire. Celebrate.

Testimonials

September 29, 2019

Differentiate. Inspire. Celebrate.

Expert views

September 28, 2019

"Throughout its history, Mauritius has always been able to re-invent itself in times of hardship."

Expert views

September 28, 2019

"Throughout its history, Mauritius has always been able to re-invent itself in times of hardship."

Expert views

September 20, 2019

"Africa is the hinterland for the Mauritian financial services space"

Expert views

September 20, 2019

"Africa is the hinterland for the Mauritian financial services space"

Expert views

June 14, 2019

What’s next for Private Wealth?

Expert views

June 14, 2019

What’s next for Private Wealth?

Expert views

May 03, 2019

“Internal audit teams should be in a position to express their views at any stage”

Expert views

May 03, 2019

“Internal audit teams should be in a position to express their views at any stage”

Expert views

April 24, 2019

"We provide connectivity to HNW South Africans investing offshore"

Expert views

April 24, 2019

"We provide connectivity to HNW South Africans investing offshore"

Expert views

April 23, 2019

Thierry Vallet, General Manager, speaks with Mauritius Golf Tours in an exclusive interview

Expert views

April 23, 2019

Thierry Vallet, General Manager, speaks with Mauritius Golf Tours in an exclusive interview

Business & Innovation

April 02, 2019

AfrAsia Bank recognised as a pioneer in the Digital HR Space by Oracle

Business & Innovation

April 02, 2019

AfrAsia Bank recognised as a pioneer in the Digital HR Space by Oracle

Expert views

March 15, 2019

There is clear visibility towards meaningful growth.

Expert views

March 15, 2019

There is clear visibility towards meaningful growth.

Testimonials

March 07, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE by Weekly

Testimonials

March 07, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE by Weekly

Testimonials

March 06, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE

Testimonials

March 06, 2019

DIFFERENTIATE. INSPIRE. CELEBRATE

Expert views

January 22, 2019

Africa will play a major role in the commercial use of financial technology.

Expert views

January 22, 2019

Africa will play a major role in the commercial use of financial technology.

Testimonials

December 13, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

December 13, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

December 12, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Testimonials

December 12, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Business & Innovation

December 07, 2018

AfrAsia Bank wins 4 awards at the EMEA Finance’s African Banking Awards 2018

Business & Innovation

December 07, 2018

AfrAsia Bank wins 4 awards at the EMEA Finance’s African Banking Awards 2018

Golf

December 05, 2018

AfrAsia Bank Mastercard Pro-Am Results

Golf

December 05, 2018

AfrAsia Bank Mastercard Pro-Am Results

Golf

December 02, 2018

Kurt kicks on with breakthrough win in AfrAsia Bank Mauritius Open

Golf

December 02, 2018

Kurt kicks on with breakthrough win in AfrAsia Bank Mauritius Open

Golf

December 01, 2018

SA's Harding chasing win number five in Mauritius

Golf

December 01, 2018

SA's Harding chasing win number five in Mauritius

Golf

November 29, 2018

Els hoping local knowledge gives him the edge in Mauritius

Golf

November 29, 2018

Els hoping local knowledge gives him the edge in Mauritius

Testimonials

October 18, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

October 18, 2018

Differentiate. Inspire. Celebrate - Weekly

Testimonials

October 17, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Testimonials

October 17, 2018

Differentiate. Inspire. Celebrate - Business Magazine

Expert views

October 10, 2018

“An ageing population is also synonymous to declining growth”

Expert views

October 10, 2018

“An ageing population is also synonymous to declining growth”

Expert views

September 28, 2018

Weekly Market Update as at 28 September 2018

Expert views

September 28, 2018

Weekly Market Update as at 28 September 2018

Expert views

September 26, 2018

Sustainability development is an essential condition to become a high-income country

Expert views

September 26, 2018

Sustainability development is an essential condition to become a high-income country

Expert views

September 21, 2018

Weekly Market Update as at 21 September 2018

Expert views

September 21, 2018

Weekly Market Update as at 21 September 2018

Expert views

September 07, 2018

Weekly Market Update as at 07 September 2018

Expert views

September 07, 2018

Weekly Market Update as at 07 September 2018

Expert views

August 31, 2018

Weekly Market Update as at 08 February 2019

Expert views

August 31, 2018

Weekly Market Update as at 08 February 2019

Expert views

August 31, 2018

Weekly Market Update as at 31 August 2018

Expert views

August 31, 2018

Weekly Market Update as at 31 August 2018

Expert views

August 24, 2018

Weekly Market Update as at 24 August 2018

Expert views

August 24, 2018

Weekly Market Update as at 24 August 2018

Expert views

August 17, 2018

Weekly Market Update as at 17 August 2018

Expert views

August 17, 2018

Weekly Market Update as at 17 August 2018

Expert views

August 03, 2018

Weekly Market Update as at 03 August 2018

Expert views

August 03, 2018

Weekly Market Update as at 03 August 2018

Expert views

July 27, 2018

Weekly Market Update as at 27 July 2018

Expert views

July 27, 2018

Weekly Market Update as at 27 July 2018

Golf

July 21, 2018

Gary Todd bags Pro-Am ticket to the AfrAsia Bank Mauritius Open 2018.

Golf

July 21, 2018

Gary Todd bags Pro-Am ticket to the AfrAsia Bank Mauritius Open 2018.

Expert views

July 17, 2018

Sanjiv Bhasin on Global Business sector: “A new market will open up”

Expert views

July 17, 2018

Sanjiv Bhasin on Global Business sector: “A new market will open up”

Expert views

July 06, 2018

Weekly Market Update as at 06 July 2018

Expert views

July 06, 2018

Weekly Market Update as at 06 July 2018

Golf

June 30, 2018

A spectacular kick-off round for a Pro-Am ticket at the AfrAsia Bank Mauritius Open 2018 at Anahita

Golf

June 30, 2018

A spectacular kick-off round for a Pro-Am ticket at the AfrAsia Bank Mauritius Open 2018 at Anahita

Expert views

June 29, 2018

Weekly Market Update as at 29 June 2018

Expert views

June 29, 2018

Weekly Market Update as at 29 June 2018

Expert views

June 22, 2018

Weekly Market Update on Radio One as at 22 June 2018

Expert views

June 22, 2018

Weekly Market Update on Radio One as at 22 June 2018

Expert views

June 13, 2018

"Mauritius is considered as one of the most stable countries in Africa"

Expert views

June 13, 2018

"Mauritius is considered as one of the most stable countries in Africa"

Expert views

June 12, 2018

Rethinking private banking

Expert views

June 12, 2018

Rethinking private banking

Golf

June 04, 2018

Sanjiv Bhasin, CEO, speaks with Mauritius Golf Tours in an exclusive interview

Golf

June 04, 2018

Sanjiv Bhasin, CEO, speaks with Mauritius Golf Tours in an exclusive interview

Business & Innovation

May 17, 2018

AfrAsia wins the Best Corporate Bank 2018 award for the second year in a row

Business & Innovation

May 17, 2018

AfrAsia wins the Best Corporate Bank 2018 award for the second year in a row

Expert views

May 15, 2018

'Mauritius has the benefit of being in Africa without being in mainland', says Assad Abdullatiff

Expert views

May 15, 2018

'Mauritius has the benefit of being in Africa without being in mainland', says Assad Abdullatiff

Expert views

May 15, 2018

IFRS9 - What you need to know by Robin Smither

Expert views

May 15, 2018

IFRS9 - What you need to know by Robin Smither

Business & Innovation

May 15, 2018

Banking on customer centricity

Business & Innovation

May 15, 2018

Banking on customer centricity

Community

May 15, 2018

Supporting the communities where we live and work

Community

May 15, 2018

Supporting the communities where we live and work

Events & Webinar

May 15, 2018

AfrAsia Bank Roadshow: Johannesburg business elites under one roof

Events & Webinar

May 15, 2018

AfrAsia Bank Roadshow: Johannesburg business elites under one roof

Events & Webinar

May 15, 2018

AfrAsia Bank Real Estate Seminar: The property investment hotspots revealed

Events & Webinar

May 15, 2018

AfrAsia Bank Real Estate Seminar: The property investment hotspots revealed

Events & Webinar

May 14, 2018

AfrAsia & SA Chamber of Commerce host futurist expert, Anton Musgrave for thought-provoking experience

Events & Webinar

May 14, 2018

AfrAsia & SA Chamber of Commerce host futurist expert, Anton Musgrave for thought-provoking experience

Business & Innovation

January 01, 0001

A clientele made up of 70% foreigners

Business & Innovation

January 01, 0001

A clientele made up of 70% foreigners