I don’t think you can get to be a really good investor over a broad range without doing a massive amount of reading. I don’t think anyone book will do it for you.

USD

EUR/USD

The Shared currency pared gains to $1.1034 as Ukraine's woes intensified ahead of ECB's Lagarde and Fed's Powell's speech.

GBP/USD

The Cable firmed at $1.3154 as the Bank Of England has been aggressively tightening its liquidity despite the intensifying fears of stagflation in Europe, U.K.'s CPI eyed for this week.

USD/JPY

The Japanese yen slipped to 119.26 per U.S. dollar as a pickup in the USD demand provided an additional boost to the greenback on a closed Japanese market.

AUD/USD

The Aussie dollar darted higher to $0.7398, underpinned by rising bond yields, with Australian 10-year yields up in the past two weeks at 2.55%.

USD/CAD

The Loonie cheered to 1.2611 against the U.S. dollar on firmer prices of Canada's key export item, WTI crude oil, amid supply crunch fears due to the latest geopolitical tensions.

USD/ZAR

South African rand weakened to 15.00 against the greenback as investors assessed the impact of the start of the U.S. Federal Reserve's rate tightening cycle this week, and commodity prices such as gold fell.

USD/MUR

The dollar-rupee stayed put at 44.10(selling).

11:30 - EUR - ECB President Lagarde Speaks

20:00 - USD - Fed Chair Powell Speaks

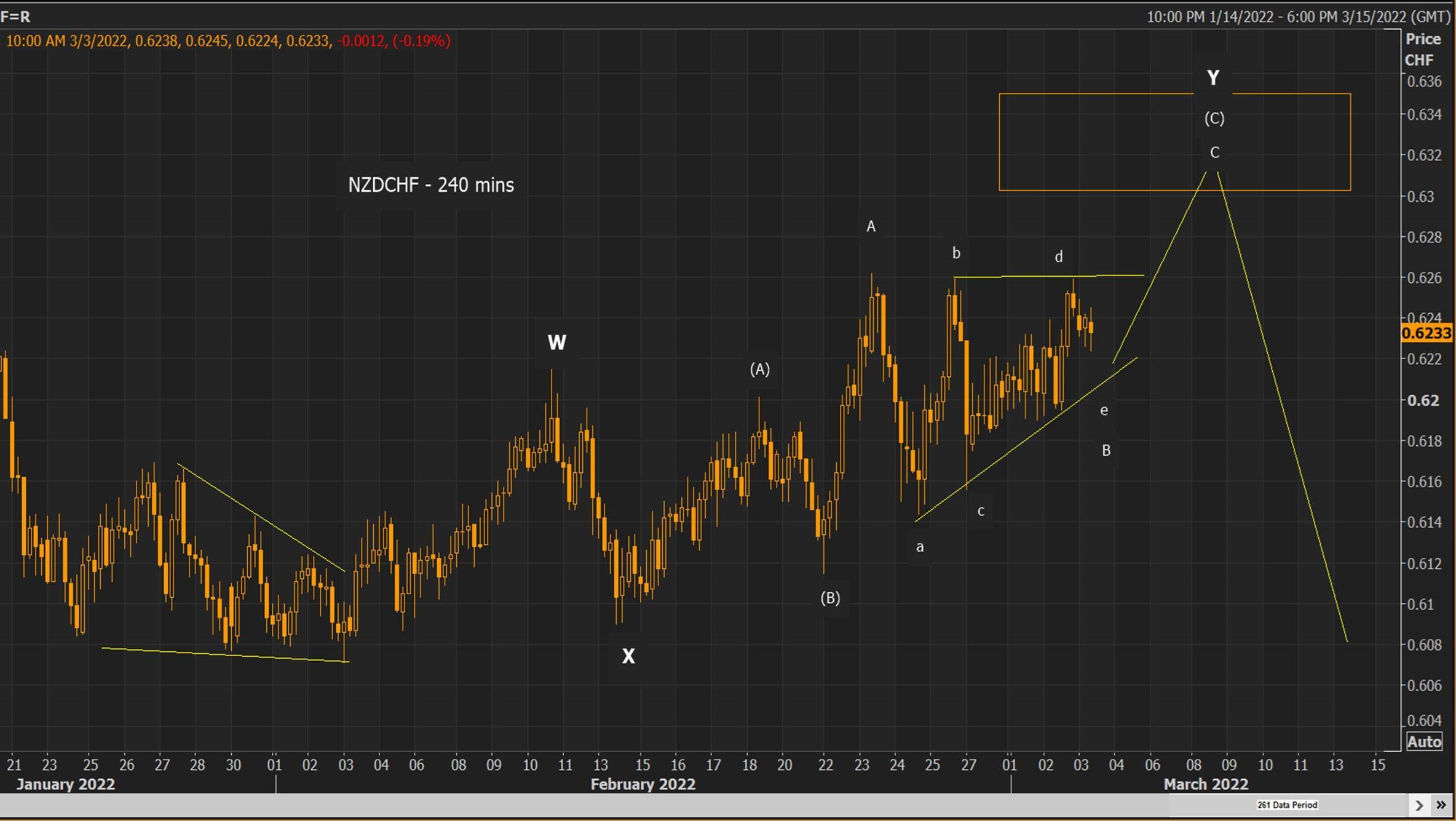

After bouncing back from key resistance level 0.6262 from the upside as per our last forecast (see below) , NZDCHF sworn down to 0.6144 but lacked sufficient selling pressure to continue its downtrend.

It appears that final wave Y of W-X-Y correction is quite complex and there might be 2 scenarios popping up in the near term.

Scenario 1 : we could have reached final wave ‘e’ before downtrend resumes. (As per Elliott wave principle a triangle can be formed as final wave C of wave Y of W-X-Y correction)

Key resistance level is wave ‘e’ of barrier triangle of wave C – 0.6259.